Major market analysis: The Spanish on-trade is decentralized, highly fragmented and rapidly going digital

In what way is the Spanish on-trade market unique in the context of Europe? What are its peculiarities? Which places are strong in which regard and where are the pockets of growth? Since SharpGrid started covering Spain this year, we’ve decided to take a closer look at the Spanish on-trade that might help our clients and potential partners in Spain better understand it and gain an advantage over their competitors. If you're interested in numbers, charts and interactive maps of Spain, keep reading.

1-MINUTE-READ: ARTICLE SUMMARY

The Spanish on-trade is an exceptionally large and important sales channel. Spanish families spend 2x more money on the on-trade than the EU average and about 60% of Spanish workers regularly eat out during their workday. Spain is also the country with the most bars per capita in the world! Despite its already large size, long-term, on-trade is expected to continue to grow with a 1-2% CAGR with most opportunities in mid-sized cities and tourism-intensive destinations. The channel is digitizing fast, both in terms of customer-facing functions (marketing, ordering, payment, etc.) as well as outlet operations (stock management, purchasing, etc.) but remains heavily fragmented with over 90% of outlets (or points-of-sale) having independent ownership.

Diving deeper, the Illes Balears province has the highest concentration of on-trade outlets per capita (1 for every 99 people) while the Comunidad de Madrid province has the lowest (1 for every 196 people). Interestingly, just 3 of the Top 60 cities with the highest concentration of outlets have a population of over half a million, indicating that most channel potential is in medium-sized cities. In fact, cities with the highest on-trade concentration have a population of just 180 000 on average. And cities with highest concentration of bars and cafés have a population of 160 000. Similarly, contrary to most markets in Europe, the capital, Madrid, is not amongst any of the top places for on-trade opportunities. The tourism-intensive destinations have the highest concentration of bars and cafes - like Santiago de Compostela, the city with the highest café concentration in Spain.

When looking at the customer engagement with on-trade outlets (measured by the amount of digital engagement like leaving reviews, commenting, rating, etc.), the top cities are Benidorm, San Bartolomé de Tirajana and Calvià, making them (potentially) ideal places for showcasing products, test portfolio innovations etc. The “Top 5 engaged cities” all have a population under 100 000, further strengthening the hypothesis about the decentralized and fragmented nature of Spanish on-trade.

—

SharpGrid Outlet Census is a BI tool available in Spain since July 2022, but we have been analyzing and scouting the market long before that. Thanks to that, we now have access to comprehensive data about the Spanish on-trade so we decided to put them to use and do a proper assessment of its specifics, conditions and interesting facts.

For this article, we are joined by our Spanish Market Research Lead and Business Development Specialist Elena García Vargas who is spearheading our expansion to the lands beyond the Pyrenees. We will start with third-party data for economic and sociological context and get to Outlet Census data visualized in an interactive map in the main section of this article.

General on-trade overview and customs in Spain

One of our first aims was to determine how important the on-trade channel is in Spain. We presumed it would play a big role, but were still surprised by the numbers. For example, according to an MDPI market assessment report, Spanish families put 15% of their money into on-trade.

“That is almost twice the average of the European Union and over three times more than German families spend on dining or drinking out in terms of family budget share,” says Elena, quoting the MDPI market assessment report.

What’s more, a recent study by the Federation of Independent Users and Consumers states that about sixty percent of workers regularly eat out during the workday and of these almost seventy percent relies solely on lunch menus that these restaurants offer. And what about drinks? Spain also excels in this respect.

“Not many people know this but according to the Spanish National Statistics Institute, Spain is also the country with the most bars per capita in the world,” says Elena. “One of the things that we have done the most with my parents growing up, and that is a very Spanish thing to do, is the aperitivo. We would go for the aperitivo every weekend and, when on holidays, especially summer, basically every day.”

In other parts of Europe and the world, it is very common to meet with friends at home for a few drinks or a barbecue in the garden. But not so in Spain, as Elena puts it: “When we meet someone, we do it most of the time in a bar or a café rather than at home. I would say that in Spain life happens mostly out of home instead of at home.”

A closer look at Spanish on-trade: Fragmentation, tourists and rapid digitization

According to a report from a research company Mordor Intelligence (don’t be fooled by the name, it has nothing to do with rings of power), there is an expected growth of 1.28% CAGR during the next 5 years and the biggest pockets of growth will be located in small to mid-sized cities with opportunities for getting products in front of the right people.

“You see, the Spanish on-trade is not concentrated in big cities like in other European markets. You have a lot of small towns or even villages along the coast that might not have big population counts but are visited by loads of tourists, especially during the summer months. So it’s much more fragmented,” adds Elena.

The potential customer universe is fragmented even on the ownership level with most outlets (be it restaurants, bars, cafés or other points of sale types) operated by independent owners, often family businesses and so on. According to the aforementioned report, these account for more than 90% of sales in this channel.

Another thing to consider is the number of tourists coming to Spain every year. Just before the covid pandemic hit the world, the country was visited by about 80 million foreign tourists, not to mention internal tourism. So even though some towns might look insignificant in terms of population, they are actually opportunities for those who know where to focus their resources.

“For example, there is a city called Logroño which has become a very popular destination for bachelor parties,” says Elena. Insights like this are achievable only by a combination of native Market Research Leads, that’s why SharpGrid has a dedicated person for every market we’re in.

Last but not least, there is a growing importance of digitization of the foodservice in Spain. Outlet owners advertise on social media, users leave ratings and reviews, delivery apps (read our article on the importance of approaching these in the right way) are still going strong even though the worst of the covid waves are hopefully behind us and so on. And this is exactly where SharpGrid enters the stage to harness the power of this digital revolution and make sense of the millions of data points it generates every day.

“The on-trade in Spain has experienced a huge development in terms of digitization, especially because of the pandemic. It has also been shown that in order for an outlet to survive in the Spanish HoReCa sector, it has to have an online presence,” adds Elena.

Which Spanish provinces have the strongest on-trade market?

If you don’t know SharpGrid Outlet Census, it’s a tool that allows sales departments to effectively target the best on-trade outlets for their products or brands with the ultimate purpose to get more from their resources and boost their ROI as much as possible. Read the Outlet Census product page to get into more details. Now let’s have a look at the data.

We started on the high level and asked ourselves: Which provinces have the biggest on-trade potential in terms of outlet count per capita? We are excluding the two enclaves Ciudad de Ceuta and Ciudad de Melilla given their small size in order not to distort the overall picture of the on-trade market in Spain.

The clear winner is Illes Balears with 1 outlet for every 99 people and the loser is Comunidad de Madrid with 1 outlet per 196 people. This can be attributed to the sheer size and population of Madrid agglomeration as the location of the country’s capital. On the other hand, Illes Balears have only ⅓ of Madrid’s population, but are very popular as a tourist destination, therefore having a strong on-trade presence. Even though on-trade is strong in Spain even in non-touristy places. As Elena says: “It is culturally embedded in our social behavior.”

Spanish cities and their on-trade opportunities

But let’s go even deeper on the level of individual cities where things start to get even more interesting. The fact that only 3 of the 60 cities with the highest concentration of on-trade outlets and potential have a population of over half a million speaks for itself: Málaga, Seville and Barcelona. The rest of the on-trade heavyweights in Spain are smaller cities with an average population of around 180,000 inhabitants. This analysis confirms our earlier point about the strong decentralization / fragmentation of the Spanish on-trade channel.

Most of the on-trade heavy cities are located either close to the coast or on the island regions. Just take the winner Calvià with 128 outlets per 10 000 people, for example. It’s a rather small city with around 50 000 inhabitants, but has over 20 beaches and is visited by over 1.6 million tourists every year, so the on-trade is naturally very strong here.

This is the finest example of why targeting is important. Without data, you might dismiss the place as unimportant, given the small population and distance from big cities. But knowing the outlet per capita density and tourist numbers gives you a first indication that this specific city might be worth exploring further.

Data highlights and peculiarities at provincial level

Our next question was a bit more complicated than that: How are different types of outlets distributed amongst the provinces? Is there one with a really strong bar scene (and therefore ideal for e. g. spirits producers) or one that has a high percentage of hotels and therefore is affected disproportionately by tourism?

First, let’s look at the national average for the whole of Spain. The outlet type ratio is as follows:

.png)

If you’re not from Spain, you might be wondering why the “pub” category is missing. The reason is simple: It’s because of different naming conventions in Spain as opposed to e. g. Central Europe. In Spain it’s common to use the term “bar” even for places that would be called pubs in some other countries like Poland, Germany or Czechia. And even though SharpGrid Outlet Census has separate categories for each of these, we have merged them for the purpose of this article in order to respect the local customs.

Going down to the province level, we have spotted several peculiarities. Firstly, there are 4 provinces where restaurants account for more than 40% of outlets:

- Comunidad de Madrid with 42%

- Illes Baleares with 43%

- Canarias with 42%

- Cataluña with 42%

If you’re a beverage producer for example, with a higher restaurants ratio you can expect on-trade outlets and points of sale in these provinces to be more after drinks that pair well with food such as non-alcoholic drinks, beer or wine, rather than hard liquor or spirits in general.

There are 5 provinces with a much higher ratio of accommodation-type outlets (typically hotel restaurants etc.):

- Aragon with 12%

- Cantabria with 12%

- Castilla-LaMancha with 12%

- Castilla y Leon with 13%

- Extremadura with 13%

And on the other hand 3 with a really low count of accommodation-type outlets:

- Comunidad de Madrid with 7%

- Comunidad Valenciana with 7%

- Regione de Murcia with 6%

This might seem strange at a first glance given the size of Madrid and Valencia provinces, but it’s not about the total number, but their ratio. It might indicate to you that Madrid and Valencia are catering more to different types of people (there are a lot of students, working people, families etc.), whereas accommodation-heavy provinces might provide more tourist hotels and related on-trade services, but fewer bars or pubs for locals.

We had a hypothesis that most of the fast food restaurants would be located mostly in provinces with the biggest cities, and this has proven to be true as the highest concentration was in these 2 regions::

- Regione de Murcia with 4%

- Comunidad de Madrid with 4%

Madrid is obviously the biggest city in Spain and Murcia is also one of the largest settlements in the country with a population over half a million people.

The business impact for Spanish on-trade producers

We see that the main on-trade centres in Spain are not concentrated within the bigger population agglomerations. Rather, they tend to concentrate in places with a high proportion of tourists. And it also shows the social behavior of Spanish people.

Elena adds: “Seeing provinces categorized based on their outlet types brings a very interesting insight regarding the main focus of each one of these provinces, not only economically but also socially speaking, and I do believe this perspective is something that would be very important to understand when trying allocating resources depending on the necessities of each one of our clients.”

This approach is fundamental for better understanding of the trends and market evolution, which is necessary to better predict the future behavior of the sector in order to adapt and quickly come up with strategies allowing brands to grow in sales and visibility perspective.

Bars in Spain and where to find them

We were also curious about which part of Spain would have the highest concentration of bars since Spain is known globally as the country with the highest concentration of bars in the world. Our guess was big cities again, but same as with the previous example, this proved to be wrong as the biggest ratio of bars was in País Vasco (30%) and the least in the Canarias (19%). Looks like Canarias is more of a family than partying location.

“It makes sense because there are places like San Sebastian or Bilbao located in País Vasco which are very popular with tourists,” explains Elena. “San Sebastian has one of the most known beaches in the entire country and hosts international film and jazz festivals attended by celebrities which gives this place a special allure. Bilbao has the famous and internationally known Guggenheim museum. Additionally, both of these cities have a very famous Basque tradition of "los pintxos", considered to be the king of tapas in the rest of Spain. Most of their tourism comes from that, their marvellous landscapes and their beaches which are well known for surfing,” explains Elena.

Looking for the "Party capital" and "Café capital" of Spain

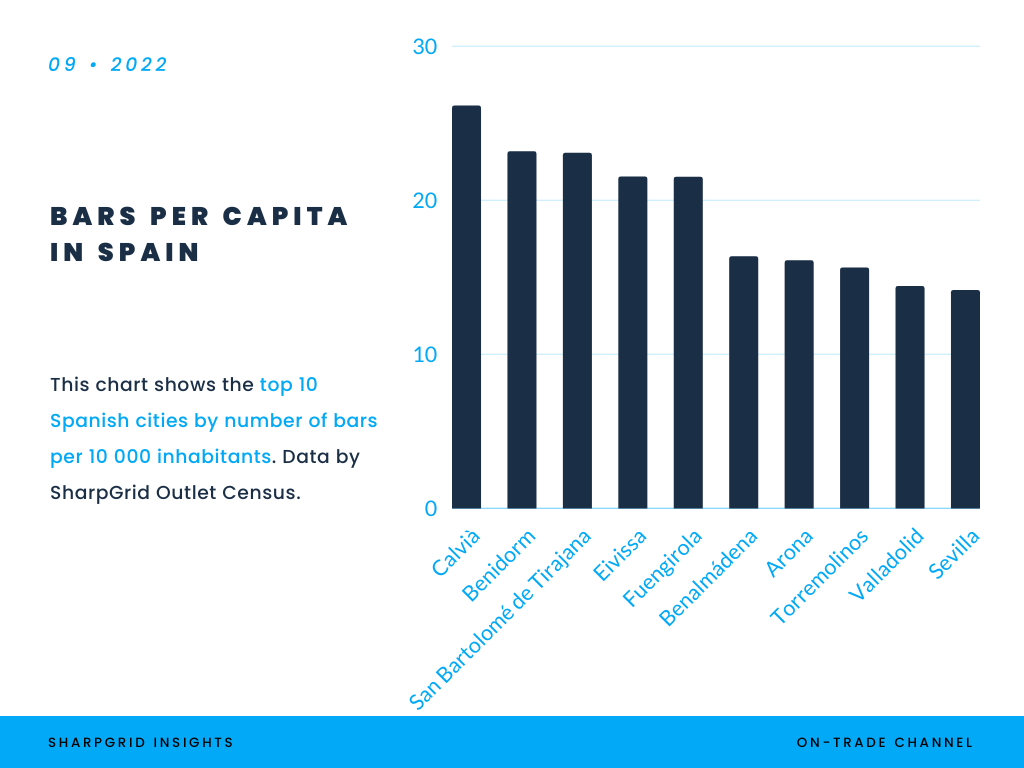

But let’s go even deeper again and look at which cities are “meccas” or “capitals” of certain outlet types. Our first question was: Which city is most heavily populated by bars and therefore is the “party capital” of Spain?

The winner is once again Calvià and the broader list is quite similar to the list of general on-trade outlet heavyweights. It seems that big on-trade places cater more to party-goers or tourists who want to have fun with spirits and cocktails in bars rather than quietly chat at a café.

Note that have merged the bars and pubs category as in Spain they are very often interchangeable and may signify a similar type of outlet.

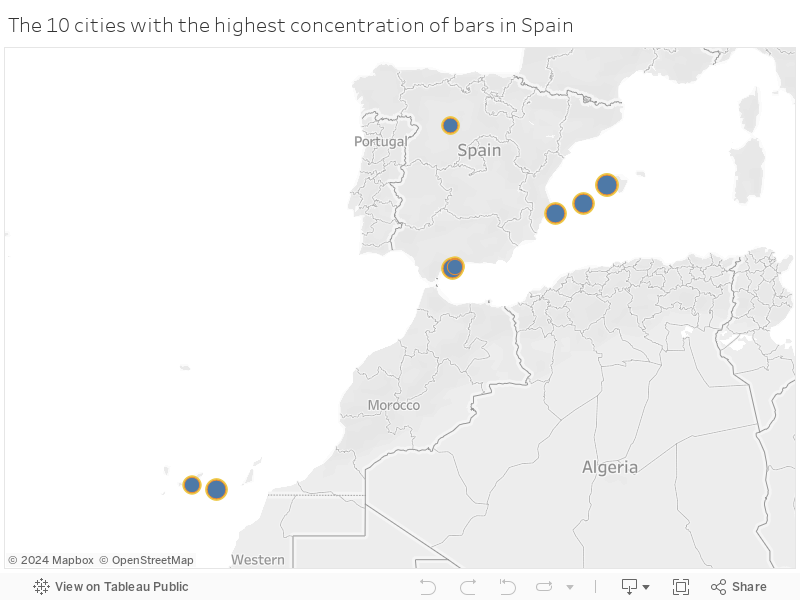

Here's a map with the top 10 Spanish cities by bar per capita. Notice they are located mostly in places popular with tourists, especially on the islands or seaside. There is even one huge "party zone" in the south with 3 cities - Benalmádena, Fuengirola, Torremolinos - next to each other (to see it properly, zoom in on them in the map).

Map: Use mouse wheel, touchpad (2-fingers scroll) or double-click to zoom in. Hover over the circles to reveal detailed data.

But there is another way to look at the “Party capital” and that is through the lens of discotecas or disco clubs which are actually considered the proper party places as they often stay open throughout the night till early morning. Here is the chart:

After comparing the disco and bar charts, you will notice that the cities mentioned are almost identical, just in a different order. This further strengthens the idea that these cities have the biggest concentration of partygoers and might be ideal targets for alcoholic drinks producers.

After cross referencing all the data from pubs, bars and discotecas, we can conclude that the ultimate winner and the “party capital” of Spain with the highest concentration of party-type outlets per capita is Calvià.

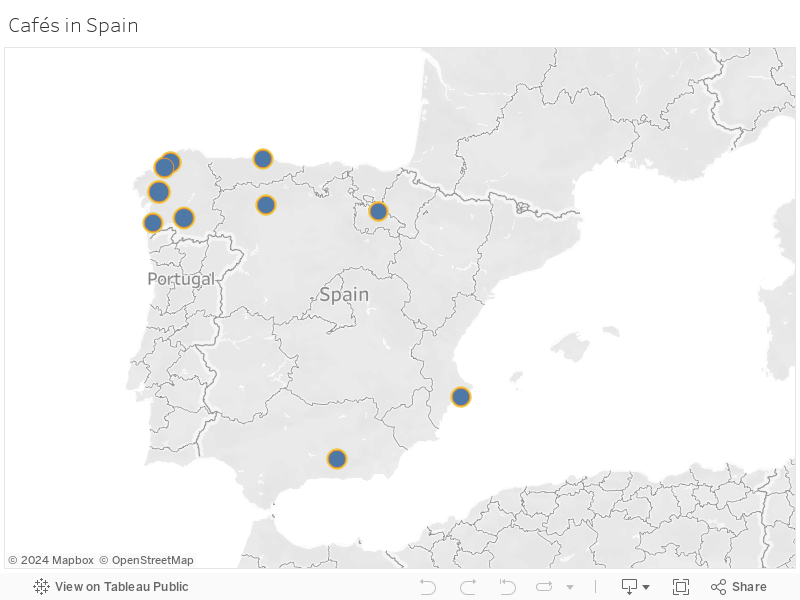

This leads us to our second finding regarding the so-called “café capital” of Spain.

Outlet Census data show that cities with a high number of cafés per capita are concentrated in different places and not as much on islands and beaches like bars. The clear winner here is the province of Galicia. See the map:

Map: Use mouse wheel, touchpad (2-fingers scroll) or double-click to zoom in. Hover over the circles to reveal detailed data.

But as for the city size, the average population is very similar to the overall average population of on-trade-heavy cities: 170 000 for bars and 150 000 for cafés. This further supports our thesis about the fragmentation of the Spanish on-trade channel.

Spanish on-trade vs other European countries

The capital city of Madrid did not even make it into the top 60 (66th place for bars, 113th place for cafés and last place for outlets per capita in general). Compare these 2 charts:

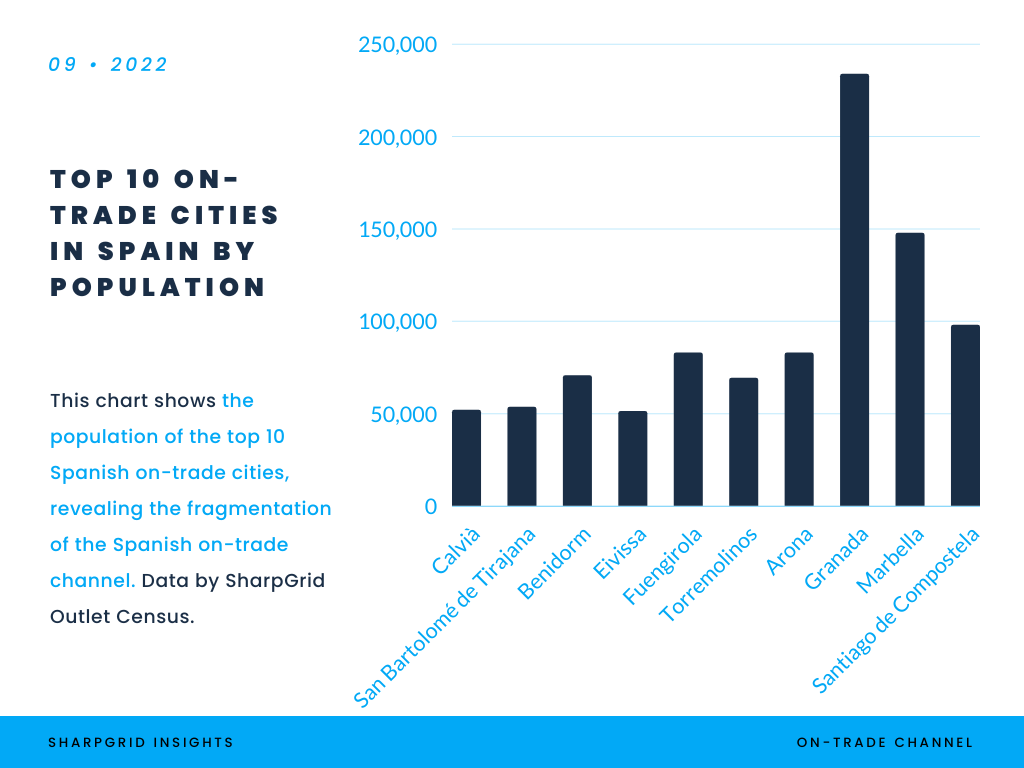

.png)

As you can see, the cities with the highest on-trade concentration are no metropolises. In fact, most of them have population under 100 000 people. The biggest one is Granada with a population just over 200 000.

This gets especially interesting if you compare Spain to Central Europe. We did similar (lower-scale) research on Czechia, Poland and Slovakia and in all 3 cases, the capital was always in the top 5 and most of the bar-heavy places were also located in the largest cities. The case is almost the same for total outlet count per capita.

We have even discovered a pocket of local on-trade concentration in Poland away from the big cities along its northern Baltic sea coast (see our Hot Zones research for more information), but even those places lagged behind the biggest cities like Kraków, Poznaň or Warsaw. Completely different case than in Spain.

“Even though I was expecting a fragmented on-trade sector, I was definitely not expecting at all to not have the biggest cities within this chart, especially when talking about Madrid,” says Elena. “I thought it was also quite cool to see that the cities with more cafes and those with more bars differ in terms of geographical localisation, and it seems that while bars are located mostly on the coast, cafes are mostly located in the north, which could also be related to the different types of climate that characterize these regions.”

How engaged are Spanish on-trade consumers?

One of the most useful indicators in Outlet Census is Consumer Engagement which aggregates digital likes, ratings, followers and other interactions on platforms like social media, travel portals, digital maps like Google Maps and so on. We looked at which cities are the most engaged and wondered if the numbers would match previous data.

.png)

As you can see, the cities with the most engaged consumers are roughly similar to the top on-trade heavyweights with the winners being: Benidorm, San Bartolomé de Tirajana and Calvià.

Outlets in these cities, therefore, generate the most “buzz” and one can expect them to be exceptional places for on-trade producers and vendors to showcase their products, test portfolio innovations or build their brands. The first 5 top engaged cities all have a population under 100 000, further cementing our fragmentation thesis.

Implications: The importance of precise outlet targeting

There is one clear lesson from all this: if you as an on-trade producer or vendor really want to find out which places are worth your attention, you need to have accurate data and know how to use it.

The SharpGrid Outlet Census is a tool designed to do just that - it's powered by our granular data, but it's also easy to pair with CRM systems or use in the form of an interactive map so that it's simple to use for anyone, whether they're a digital-first kind of person or a someone who prefers less interactive tools.

Only by being able to see in detail which places offer the most opportunities can you streamline your sales, get more customers and manage sales teams effectively. But Outlet Census is useful in other instances, such as strategy making or investment decisions. Just look up your target outlet’s quality and see if it really makes sense to invest in it or not. You don’t want to be wasting money and time on sub-par outlets and points of sale. Give your market research a much needed boost it deserves.

And lastly, it can even help you get rid of some of the hidden costs plaguing the on-trade market that are eating away at your commercial budgets. The ultimate goal of Outlet Census is to increase your ROI and profits. See how our clients like Heineken or Unilever use it and what it has done for them. And if you’re interested in what Outlet Census can do for you and your company, contact our regional Business Development Lead Elena García Vargas (or Martin Lenc in English, if you’re not Spanish).

SharpGrid is a data & tech company reinventing market research in the on-trade channel. The on-trade channel consists of POSs (points of sale) like restaurants or bars where food & beverage is bought and consumed, and is often also called HoReCa, on-premise, food service, out-of-home, gastro or immediate consumption (IC) channel, hospitality or on-licence.