Czech Beer Special: Volume & Value data shows rising consumption and price with strong regional leaders crushing the market

Our new addition to Market Meter, the Volume & Value Dashboard, has delivered its first results, so we thought we'd share the highlights with you. We'll focus primarily on changes in volume & value over the past quarter and year-over-year, as well as brand strength by region.

Current beer volume & value in the Czech on-trade

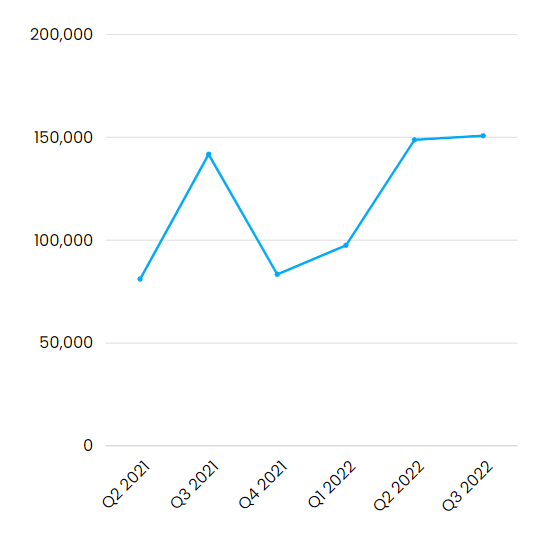

We'll start by looking at the top - that is, the on-trade beer market as a whole. After the sharp covid declines (the whole channel was closed for a prolonged period of time), the volume appears to be returning to more favorable levels.

The second quarter of 2022 saw volume almost double that of last year, and the third quarter added even more: + 1.34% and + 6% year-on-year. For more details, see the chart below (calculation unit: 1000 l of beer).

The growth figures this year are consistent with a strong spring and summer season.

The value chart (calculation unit: 1000 CZK ≈ 40 €) looks almost identical but shows higher fluctuations compared to volume. This is most likely due to the arrival of inflation and rising producer prices reflected in the consumer price of beer.

Q2 2022 vs 2021 was almost double (same as with volume). The third quarter of 2022 then saw a 4% increase over the second. Year-on-year, the total value in the Czech beer market increased by 13%.

Overall, we see on-trade beer consumption increasing steadily so far despite the adverse economic conditions and we will be eagerly awaiting the next quarter's figures which should see the impact of full-blown inflation, the energy crisis and the coming recession. We are convinced that the Czechs will not let go of their national treasure even in hard times.

The power of Czech beer brands in the regions

A specific phenomenon in the Czech HoReCa market is the regional strength of Czech beer brands. The strength of even relatively large brands fluctuates region by region, often to very extreme values.

First, we looked at 3 “universal” brands. Pilsner Urquell is a world-renowned brand that should have a similar market share in all Czech regions. Its overall volume share in the country was 22%, with only two regions significantly below this average - Moravian-Silesian (15%) and South Moravian (16%), where the strength of local brands is more evident.

The Birrell brand has a similarly universal position in the Czech Republic, with a national average volume share of 9% and the only significant fluctuation in the Pilsen region (15%).

Bernard may also be considered “universal” with an average of 4% and just four larger fluctuations - the brand is stronger in Vysočina (8%) and weaker in Pilsen, Liberec and Karlovy Vary (all three 2%).

Local leaders are beating the market

Now, let’s dive into the regional specifics.

Ostravar has a volume share of 5% in its home Moravian-Silesian region, while in the other regions, it oscillates between zero and one percent. It also makes 78% of its sales in its home region.

Starobrno is in a similar position: 11% in its home South Moravian Region, 8% in the Zlín Region, 2% in the Olomouc and Vysočina Regions (all nearby South Moravia), and virtually unheard of in the rest of the country. It sells 68% of its production in its home region, 19% in Zlín region and only fractions of percent in the other regions.

Even Březňák from Ústí nad Labem was no surprise, with 10% in its home region, 2% in South Moravia and not even one percent in any other region. In Ústí nad Labem, 55% of sales are made in the region, and 26% in South Moravia.

Budvar has an Ús11% volume share in its home South Bohemia region and 0-3 % in the rest of the country, with the smallest share in the Pilsen region (0,83 %). However, its sales are much more spread out between the regions. The highest share is in South Bohemia - 28 %. This is followed by Prague with 14% and the South Moravian Region with 10%. The rest of the regions are between 1-8%.

Central Bohemian Krušovice thrives in Ústí nad Labem and Karlovy Vary, but is strongest in the South Moravian Region (4%). This apparent anomaly can be explained by the synergy with the Starobrno brand, which pushes the Krušovice brand upwards even this far from its home base. The South Moravian region also produces the most sales, namely 25%. Then in Prague 19%, in Central Bohemia 13% and the same in the Ústí nad Labem region. The other regions are in single digits.

Kozel has an interesting position. This brand is strong in the regions belonging to the Bohemian part of Czech republic, but it is weak in Moravia. In the Bohemian regions, it has an average volume share per region of 8%, while in Moravia and Silesia, it is only 4%. Most of its production is sold in Prague at 21%. It also has 15% in Central Bohemia, 9% in South Bohemia, 8% in Kralovehradecky and 7% in Liberec.

Litovel in Olomouc unsurprisingly has the largest share in the Olomouc region, namely 9%. It is followed by the South Moravian and Liberec regions with 1%. In the other regions, we hardly come across it. In the Olomouc region, it also sells 60% of its production. Similarly, Zubr from the same region has a 2% share and sells 60% of its production there.

The narrative is also confirmed by Holba from Hanušovice. It is also the strongest on its home turf in the Olomouc region with a 4% share and sells the most production there - 50%.

As you can see, except for Pilsner Urquell, Birrell and maybe Bernard, Czech beer brands are exceptionally strong in their home markets and sell most of their products there.

Beaten Big Beer Brands

An interesting finding is that even if a global distributor has a regional brand under its wing, it does not mean that it has to succeed in breaking through with it in regions other than its home region. This can be seen in the example of Ostravar, Starobrno or even Radegast, which belong to international beer groups and yet are only strong in their home regions.

However, the good news for everyone is that beer consumption in the on-trade is growing despite higher prices and Czech beer brands (and their global distributors) are still going strong. Let's hope this continues to be the case in the coming quarters.

SharpGrid is a data & tech company reinventing market research in the on-trade channel. The on-trade channel consists of POSs (points of sale) like restaurants or bars where food & beverage is bought and consumed, and is often also called HoReCa, on-premise, food service, out-of-home, gastro or immediate consumption (IC) channel, hospitality or on-licence.